.svg)

All about the EU’s game-changing Corporate Sustainability Reporting Directive

CEO

Howden manages Scope 3 PG&S emissions across 55 countries with DitchCarbon.

.webp)

Executive Summary:- A new European Union law stipulates that all large companies must publicly release environmental and social impact statements on a regular basis.- This new directive builds off the Non-Financial Reporting Directive (NFRD), but goes a step further by including sustainability criteria for large companies (with over 250 employees) and making those reports publicly available.- 1 January 2025 is the deadline for companies to submit their CSRD-aligned reports for the 2024 financial year.

The Corporate Sustainability Reporting Directive (CSRD) In a Nutshell

The Council and European Parliament provisionally agreed on the CSRD on 30 June 2022. This proposal seeks to improve the current rules on disclosure of non-financial information so that investors can consider sustainable economic growth when making decisions.

The CSRD supports the European Green Deal, which is the EU’s roadmap for making Europe climate-neutral by 2050. The Directive is also in line with the Sustainable Development Goals (SDGs), which the UN has set for 2030.

The CSRD helps company investors, consumers, stakeholders, and policymakers understand how large businesses are performing beyond their financial health. The goal is to get these entities to manage their approaches to business more responsibly. For instance, it dramatically changes the way companies report on sustainable practices.

With the CSRD, the European Commission finally has a system for measuring non-financial data that can be applied across all EU member states.

Since compliance is happening on 1 January 2025 at the latest for the 2024 financial year for large companies already impacted by NFRD, companies will face challenges with reporting and data collection. Both of these tasks require heavy time and resources, which some companies might not have.

If you wonder whether or not your company needs to comply-and what steps to take to get there-we have you covered.

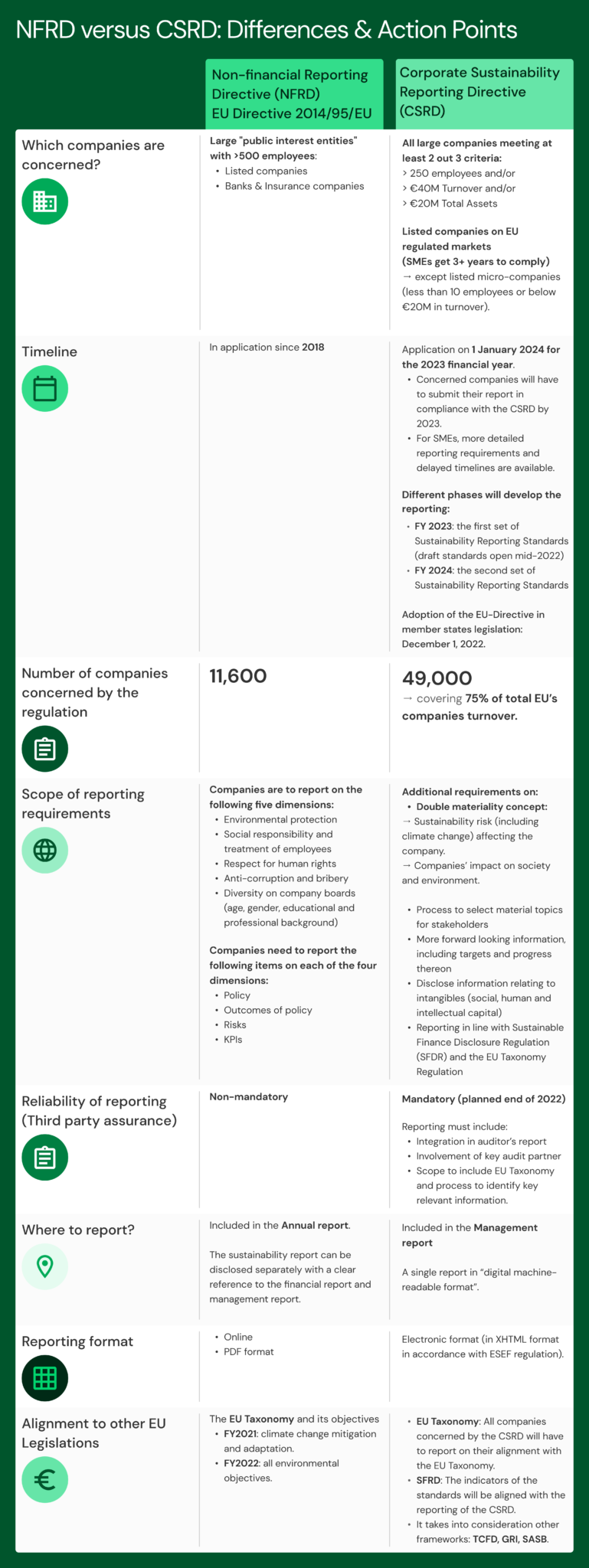

CSRD vs. NFRD: Key Differences

Aside from the differences we’ve previously mentioned, here’s a look at each of the differences between the old policies and the new ones.

Source: Plan A

When do these rules go into effect?

Depending on whether a company is listed or unlisted, different timelines apply. For companies affected by the NFRD, they have to comply with the CSRD starting from 1 January 2024 at the latest.

Which companies must comply with the CSRD?

Previously, the NFRD only required public-interest companies with 500+ employees to disclose their non-financial information. The CSRD broadens this scope to all companies with more than 250 employees that meet either two of the following three criteria:

Additionally, all listed companies (save microenterprises and companies with fewer than 10 employees or a market cap below €20 million) will have to disclose their sustainability information as part of their financial reporting.

The threshold for listed companies is important because, unlike the US, most companies were not required to report on sustainability at all in Europe. The EU’s approach is thus industry-neutral: All large companies have to provide comparable information on their sustainability performance.

This is a key distinction from the NFRD, which only required companies to disclose their non-financial information if they were public-interest entities (PIEs).

In total, the CSRD will affect an estimated 50,000 companies in the EU with over 15,000 in Germany alone. At a time when Environmental, Social, and Governance (ESG) reporting is gaining lots of traction, this accounts for about 75% of all turnover in the EU’s stock markets.

What information do companies need to disclose?

The Directive introduces several new Corporate Social Responsibility (CSR) reporting requirements for companies, most notably around climate change, diversity, equity, and inclusion (DEI), and human rights.

Here are a few important categories:

Another important factor is double materiality, which is the sum of sustainability risk (i.e., how a company’s sustainability performance could affect its business success) and the company's impact on society.

They will also need to report more information on the following:

This approach helps businesses focus on the sustainability topics that are most important to their success and determine which stakeholders they need to engage with.

How will companies report on this information?

Companies will have to consider reporting frameworks for their data. The goal is for companies to provide a balanced and comprehensive overview of their sustainability performance. However, there is no one-size-fits-all solution here. The type and format of data disclosure will depend on the company’s size, sector, business model, and sustainability strategy.

The Directive requires companies to use recognized sustainability reporting standards to make sure that the information disclosed is comparable, transparent, and reliable. The European Financial Reporting Advisory Group (EFRAG) will be in charge of European standards, after receiving technical tips from a few different European agencies.

See the EFRAG reporting standards for the CSRD.

What the New Directive Means for Companies

For companies to find success and remain compliant, it'll take more than just learning how to identify and gather climate-related information. Organizations will also need to establish policies, set targets, and KPIs that help manage ESG risks-and they'll need to do all of this quickly.

Particularly for companies that don't have sustainability reporting experience, the transition will require lots of effort and coordination between different teams, including finance, accounting, investor relations, sustainability, communications, legal, and audit.

But with the right approach, the benefits of sustainability reporting can outweigh the challenges. It can help build trust with investors and other stakeholders, attract new talent, manage risks more effectively, and make better business decisions.

Costs of Sustainability Reporting and Tracking

Although the EU states its goal is to make sustainability reporting "cost-effective," the reality is that it will likely come with additional costs for companies-at least in the short term. These could include:

The good news is that, as more companies adopt sustainability reporting, the cost of compliance is expected to go down.

Management Expectations for CSRD Compliance

Companies under the scope of the Directive will place responsibility on management to ensure disclosure of sustainability information in the financial statements.

In addition to staying up to date with new policies and laws, management will need to:

The board of directors or equivalent body will need to:

The Directive also requires companies to disclose how they have taken into account the interests of stakeholders when preparing their report.

KPIs to Track to Ensure CSRD Compliance

A few KPIs that companies might want to consider tracking are:

Depending on the company, industry, and size, different sustainability metrics will be more important. The key is to identify the most relevant KPIs and track them over time to ensure compliance with the CSRD

Final Thoughts

The EU's new Corporate Sustainability Reporting Directive is a game changer that will have a wide-reaching impact on companies, investors, and other stakeholders. And while the Directive is not yet in force, companies should start preparing for compliance now. This means understanding the requirements of the Directive, tracking relevant KPIs, and putting systems in place to gather the necessary data.

By taking these steps, companies can be sure that they are ready to meet the new reporting requirements when they come into effect.

Recent posts

Join the industry leaders and solve your Scope 3 emissions data challenge

See how DitchCarbon can transform your sustainability journey with auditable insights and verified data.